VC Angle Weekly Briefing #37: Europe Hits 5 New Unicorns in 2026

VC Angle Weekly Update #37

Hey - welcome to the thirty-seventh edition of VC Angle Weekly Updates! We’re moving weekly briefings to Sundays from now on.

As always, we're keeping tabs on what actually matters across 🇪🇺 European tech, as well as relevant global tech news. If something broke the news this week and it's worth your time, it's probably below. Scroll on for the deals, reads, and reports you'll want on your radar.

In This Edition:

Five new European unicorns in January

ASML forecasts record-revenue year

Revolut founder corrects UK residency filing

European VC hits $85B despite deal drought UK tops European business environment rankings

Europe hits third-strongest year by capital but second-lowest deal count in a decade

⏱️ 3:57 Reading Time

💥 Main Events Past Week

January brought five new European unicorns: Belgium’s Aikido Security ($1B), Lithuania-rooted Cast AI ($1b+), French defense tech Harmattan AI ($1.4B), German ESG firm Osapiens ($1.1B), and Ukrainian edtech Preply ($1.2B).

Nikolay Storonsky’s family office corrected corporate filings to show UK residency after an October filing listing him as UAE resident alarmed regulators reviewing Revolut’s banking licence. The £10bn fintech has been stuck in provisional banking licence limbo for 18 months despite applying five years ago.

ASML forecasts €34bn-€39bn in 2026 sales driven by AI demand

Dutch chipmaker ASML expects sales up to €39bn in 2026 after Q4 orders doubled analyst forecasts to €13.2bn. The company is cutting 1,700 jobs (4% of staff) while customers prepare for AI-driven capacity expansion.

📰 Other News

Revolut deploys ElevenLabs AI voice agents, cutting support resolution time by 8x across 31+ languages [See here]

New AI agents social media draws attention as things get… weird [See here]

Meet the new Slush CEO [See here]

VC firm 2150 raises €210M fund to solve cities’ climate challenges [See here]

Nvidia and Alphabet VC arms back AI startup Synthesia at $4 billion valuation [See here]

Europe’s investors at Davos say capital is available but fragmentation slows scale-up [See here]

Nik Storonsky’s Quantum Light fund targets $500M [See here]

Germany captured a larger share of Europe’s venture capital than the UK in 2025 for the first time in history [See here]

👇🏼 Read some of our previous weekly reports to stay in the loop with 🇪🇺 European tech news:

💶 Where Funds Went (Or Will Go)

Startups

🇬🇧/🇺🇸 Orbital — $60M | AI platform automating real estate legal workflows.

🇬🇧 Synthesia — $200M | AI video generation; valuation doubled to ~$4B.

🇵🇱 Rainbow Weather — $5.5M | Real-time environmental/weather intelligence (hyperlocal nowcasting).

🇬🇧 Vennre — $9.6M | Private-market platform expanding across MENA.

🇩🇰 Lunar — €46M | Challenger bank funding to grow business users.

🇸🇪 Brickanta — $8M | Agentic AI for construction planning.

🇬🇧 Evaro — $25M | Digital healthcare services for consumer brands.

🇩🇪 Co-reactive — €6.5M | CO₂-negative materials tech (seed).

🇬🇧 Modern Milkman — £10M | Sustainable doorstep grocery delivery.

🇸🇪 Funnel — $80M (debt) | Debt facility to scale the marketing intelligence platform.

🇩🇪 RobCo — $100M | Factory automation robots (“physical AI”); US expansion.

🇬🇧 Sokin — £70M (debt) | Funding to support major expansion.

Venture Funds

🇩🇰 2150 — €210M | Closed Fund II (assets lifted to ~€500M).

🇩🇰 The Footprint Firm — €76M | Closed Article 9 deeptech Fund I for the green transition.

🇪🇺 b2venture — €150M | Closed Fund V (hard cap).

🇩🇪 seed+speed Ventures — €90M | Closed Fund III.

🇫🇷 daphni — €260M | Closed “daphni Blue” (science-driven European investments).

M&A 🤝

🇪🇪 Scoro → Envoice — undisclosed | Project cost visibility via AI-driven expense/bill management.

🇩🇪 finanzen.net Group → Vickii — undisclosed | AI investing platform acquired by finanzen.net group.

🇩🇪 Sword Health → Kaia Health — $285M | Acquisition.

🔍 Reads & Reports

3 European countries in Top 10 countries on quality of business environment

StartupBlink’s inaugural index ranks 125 countries on business environment for startups. US scored perfectly at #1, followed by Singapore, UK, Switzerland, and UAE. Notably, China, Israel, France, South Korea, and India—all top 20 in ecosystem performance—missed the IBEI top 20, revealing a gap between startup output and underlying business conditions.

The UK, Switzerland, and the Netherlands rank 1st, 4th, and 7th, respectively.

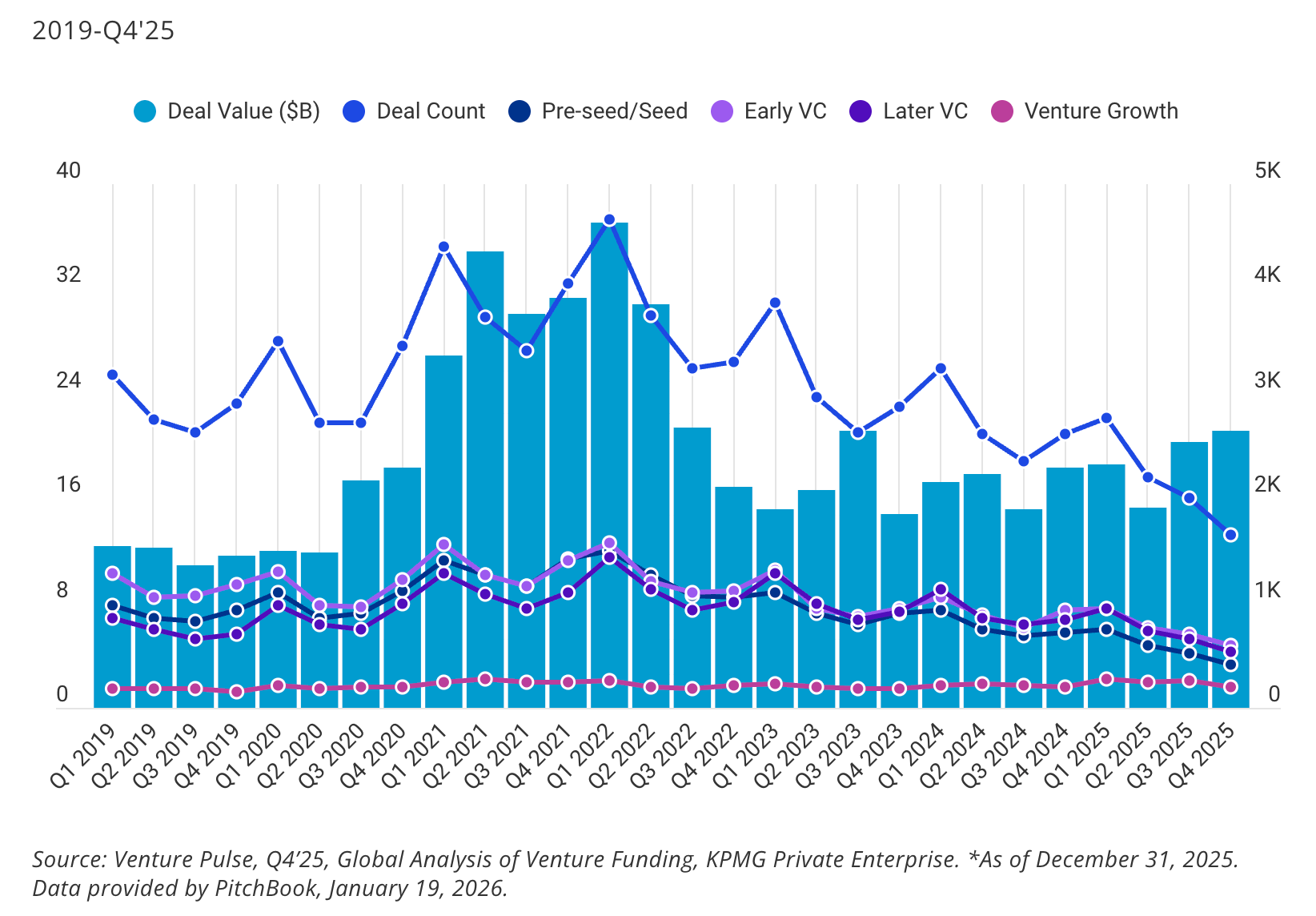

European VC hit $85.3B across 8,626 deals in 2025—third-strongest year by capital but second-lowest deal count in a decade. Q4 saw $20.7B across 1,651 deals. Capital concentrated in fewer, larger rounds: Revolut ($3B), Oura ($907M—largest healthtech raise ever), Brevo ($578M). UK led with $6.8B, followed by Germany, France, Israel. Investor focus shifted to AI application layer (Black Forest Labs $300M, Synthesia $200M) and defense tech amid geopolitical tensions. Geographic diversity strong—top 6 megadeals spread across 6 countries.

👋 That’s a wrap for this week.

If you’ve got a round, role, or resource others should see, reply to this or ping us at hello@patrons.vc or send me a message on LinkedIn. We’re bringing the best deals to our partner VCs by building Europe’s finest venture network at Patrons. If you have a good deal flow, want to expand yours, or want to reach the right investors, send us a message!

If you found this useful, send it to a founder or friend who’d appreciate it.